Singapore has become a destination country for wealthy families and family offices looking to root itself in the sunny tropical state. With 1,400 Single Family Offices (SFOs) recognised and receiving tax incentives as of December 31, 2023. This article explores the two primary routes to establishing an SFO in Singapore, exempt vs licensed family offices, along with the associated tax incentive requirements.

Routes to Setting Up an SFO

SFOs in Singapore have two primary options:

- Exempt (In-house) Single Family Office: Suitable for single family offices that hire their own investment personnel and only manages solely manages the family’s assets. If both conditions are met, the family office can be exempted from getting a financial license to manage the assets (Exempted Family Office). This option offers the benefits of independence and control over the management team, but comes with higher operational costs and longer planning.

- Partnership with a CMS License Holder: SFOs can alternatively collaborate with a licensed Capital Markets Services (CMS) firm, removing the need to establish their own team. CMS licensed entities could include capital advisory firms and other family offices.

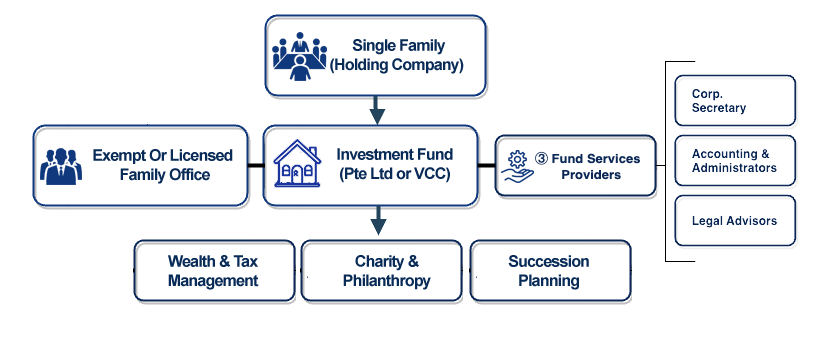

Below is an example of a typical structure whether or not the family office that manages the principal’s assets decides to use an in-house (Exempted Family Office) management team or partner with a licensed manager.

Family Offices will almost always apply for the tax incentive schemes in Singapore as they provide blanket exemption on investment related incomes for the SFO structure. As of 2024, the corporate income tax rate (CIT) was 17% which could be exempted. Notably, Singaporean real estate related income is not exempted by this exemption, but other countries are.

Tax Incentives: 13O vs. 13U

Singapore offers two key tax exemption schemes: 13O and 13U Tax Exemption Scheme.

- 13O Tax Exemption Scheme: Lower entry requirements — applicable for Singapore-based fund vehicles managed by Singapore-based fund managers.

- 13U Scheme Tax Exemption Scheme: Higher entry requirements — designed for global fund vehicles (internationally domiciled structures) managed by Singapore-based fund managers.

From 5th July 2023, Monetary Authority of Singapore (MAS) has increased the tax exemption requirements for the 13O/13U depending on whether or not the family office is licensed or exempted. For the purpose of this article, we assume the SFO is looking to setup an entity in Singapore managed by Singapore-based fund managers, therefore the table below focuses on comparing the differences only between the lower entry 13O tax exemption after the MAS revisions.

For Exempt Family Offices (13O Tax Exemption)

For Licensed Family Offices (13O Tax Exemption)

Employment Pass

Eligible for 1 Employment Pass for the Principal and their dependents

Eligible for 1 Employment Pass for the Principal and their dependents

Investment Professionals

Employ minimum 2 professionals, of whom at least 1 is not a family member. Full time (more than 50% of time), relevant work experience/education as investment professionals

Covered by the CMS Licensed Entity. No additional employees required

AUM Requirement

Minimum S$20 million in Designated Investments. Investing lower of $10 million SGD or 10% of AUM in Singapore or climate related acitivites

No minimum AUM and no prescribed investments

Spending Requirement

Tiered Spending Requirement min. SGD 200,000 annual local business spending

Fixed Spending Requirement min. SGD 200,000 annual local business spending

For Exempt Family Offices (13O Tax Exemption)

Eligible for 1 Employment Pass for the Principal and their dependents

Employ minimum 2 professionals, of whom at least 1 is not a family member. Full time (more than 50% of time), relevant work experience/education as investment professionals

Minimum S$20 million in Designated Investments. Investing lower of $10 million SGD or 10% of AUM in Singapore or climate related acitivites

Tiered Spending Requirement min. SGD 200,000 annual local business spending

For Licensed Family Offices (13O Tax Exemption)

Fund can be constituted in SingEligible for 1 Employment Pass for the Principal and their dependentsapore or overseas

Covered by the CMS Licensed Entity. No additional employees required

No minimum AUM and no prescribed investments

Fixed Spending Requirement min. SGD 200,000 annual local business spending

More details and full comparison between 13O and 13U can be found here.

Decision-Making Considerations

The choice between the two routes depends on the SFO’s objectives. If the goal is to build a dedicated team in Singapore, the exempted scheme under the 13O tax exemption is ideal. However, it faces more restrictions on minimum AUM and the 10% prescribed investments. Conversely, partnering with an existing licensed entity is more flexible and cost-effective for those seeking a streamlined setup. For families who are interested in getting Permanent Residency (PR) in Singapore, family office funds with at least $50 million SGD can contribute to the GIP PR application. Read more here.

Create Legacies & Generational Wealth

Get connected with our service partner providers to inquire how you may start your family office fund and access Singapore — the preeminent financial hub of Asia